Yuh Bank – Review and Complete Analysis (March 2026) + get 50 CHF + 250 SQW

C9QK67

Review of Yuh: The Best Online Bank in Switzerland? We Compare All Advantages… Disadvantages… Banking Services… Rates… Features… Best Deals… Shortcomings… Use the Promo Code C9QK67 to Receive 50 CHF Trading Credit + 250 SWQ (With a First Deposit of CHF 500.-).

Review of Yuh: The Best Online Bank in Switzerland? We Compare All Advantages… Disadvantages… Banking Services… Rates… Features… Best Deals… Shortcomings… Use the Promo Code C9QK67 to Receive 50 CHF Trading Credit + 250 SWQ (With a First Deposit of CHF 500.-).

[Update – 27.02.2026: Introduction of the Yuh Pillar 3a offer] [Update – 06.02.2026: Improved visibility of related content (investing with Yuh + general comparison)]

YUH is 100% owned by Swissquote. It has over 200,000 users and more than 1.5 billion francs under management. The YUH app offers:

account and card 💳

a free multi-currency account (13 currencies) with CHF, EUR, and USD by default

a free Mastercard Debit card

a free virtual card for online purchases

free payments (without exchange rate surcharge)

free CH IBAN

Yuh 14+

Yuh 14+ is a free bank account without overdraft possibility for young people aged 14 to 17.

A Swiss bank account with individual CH IBAN

A free Mastercard debit card

Free cash withdrawals once a week in Switzerland (4.90 CHF abroad)

Works with TWINT

Account opening without an adult’s signature.

Free transactions and currency exchanges in 13 currencies without additional fees

Automatic transition to the classic Yuh account upon reaching majority.

savings 📈

Dedicated savings plan (with customizable goals and no management fees).

automatic recurring transfers

1% savings interest in CHF

Free and unlimited withdrawal

Possibility to open a Pillar 3a account “Yuh 3a“, with all-inclusive fees of 0.50% and a choice among five investment strategies.

trading 🤝

no hidden costs

Transaction fees of 0.50% on stocks and ETFs, 1% on cryptocurrencies.

thematic investments

38+ cryptocurrencies available

2

The Security: is YUH Safe?

Security: YUH’s guarantees

Is YUH a Bank?

– Banking services are provided by Swissquote Bank SA, authorized by FINMA. – Swiss deposit protection insurance covers up to “CHF 100” 000.- in case of bankruptcy.

Is YUH Safe?

– YUH bank user data is stored in Switzerland. – Two-factor authentication (2FA) is used for account access.

Yuh Promo Code

Use the promo code C9QK67 to receive 50 CHF in Trading Credit + 250 SWQ (with an initial deposit of CHF 500.-).

Open a YUH Bank Account – Receive 500 SWQ(7.50 CHF)

Opening an account with YUH

YUH bank is available in French, German, English, and Italian.

Who Can Open an Account with YUH Bank?

– Residents of Switzerland, Germany, France, Italy, or Liechtenstein. – Yuh is therefore accessible to cross-border commuters and non-residents. – You must be 14 years old (Neon 16, ZAK 15). – All you need is a smartphone. – No proof of income or minimum deposit is required.

To be developed: buying crypto is interesting, but crypto transfers (to and from the YUH application) should be integrated. Our opinion on Yuh bank is also that it should integrate crypto staking possibilities in its projects section.

6

Yuh Pillar 3a

Yuh Pillar 3a

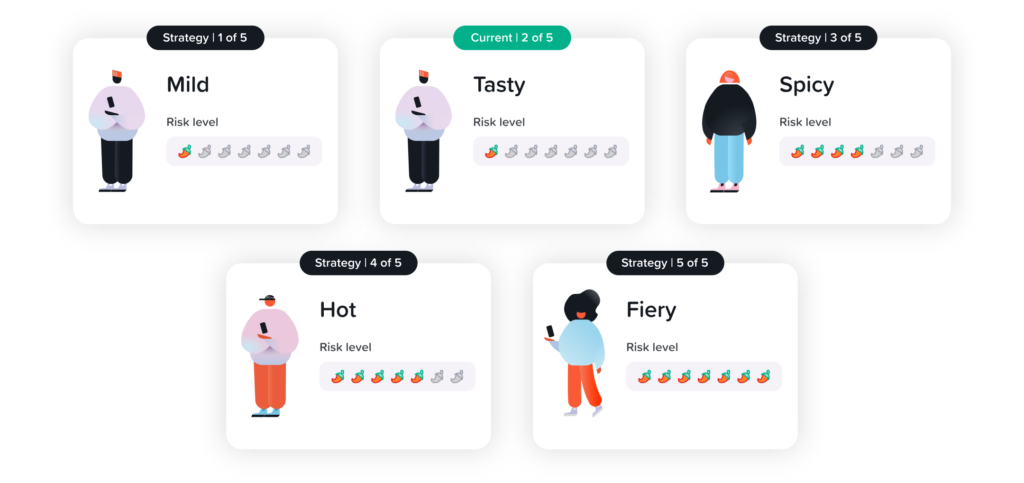

The Yuh 3a is directly integrated into the mobile app, allowing you to invest via Swisscanto index funds. It offers five risk strategies, ranging from Mild (20% equities) to Fiery (98% equities), so you can choose the risk level that matches your investment goals.

Investments can go up to 98% in equities, with the balance distributed between bonds, real estate, precious metals, and a small cash portion.

The positioning is clear: a simple 3a, all-in-one, integrated into the Yuh ecosystem, with a transparent fee structure.

Security

The Yuh 3a is based on a multi-level structure:

Descartes provides the technological infrastructure (platform and allocation).

The simply3a pension foundation legally manages the 3a assets.

Lienhardt Partner Privatbank Zürich acts as the custodian bank.

Specifically:

Assets are held via an independent 3a foundation, constituting a separate estate.

In the event of bankruptcy, the funds are not part of the bank’s balance sheet.

This structure guarantees the security of assets within the standard Swiss Pillar 3a framework, with segregated assets, a regulated foundation, and an identified custodian bank.

Conditions

Only one 3a portfolio possible

Invest from as little as 1 CHF

Standard 3a taxation

Accessible only via the mobile app

2026 legal limit: 7,258 CHF for employees with a 2nd pillar

The key point here: unlike Neon or Finpension, Yuh doesn’t allow you to open multiple 3a accounts, which limits tax optimization at the time of withdrawal.

Fees

Yuh charges 0.50% per year, all-in.

management fees

fund TER

transaction fees

currency exchange fees

stamp duties

unlimited strategy changes

The structure is simple and transparent, with no hidden fees.

However, the funds used are not specifically optimized for pensions, resulting in an estimated loss of 0.15% per year due to foreign dividends. This isn’t an extra fee, but an indirect impact on performance.

Additionally, portfolios are heavily hedged in CHF, which reduces currency risk but limits exposure to foreign currencies.

Yuh 3a is right for you if:

You want to centralize your finances in the Yuh app.

You’re looking for a simple solution with all-in fees.

You’re comfortable with up to 98% equity investment.

You don’t plan on opening multiple 3a accounts.

It will be less suitable if:

You want to optimize your taxes via multiple 3a accounts.

You want to avoid CHF hedging.

You’re looking for a more cost- and performance-efficient fund structure.

The Yuh Pillar 3a stands out for its simplicity and integration into the Yuh ecosystem, offering a turnkey solution for users who want a simple investment with clear, transparent fees. However, its lack of flexibility regarding multiple 3a accounts and its CHF hedging strategy may not suit those looking to optimize their taxes or further diversify their currency exposure.

If you’re a user looking to centralize your investments in a single app with all-in fees, the Yuh 3a is a solid option.

Can I open multiple 3a accounts with Yuh?

No. Only one 3a portfolio is possible.

Can I choose my own funds with Yuh 3a?

No. You choose a strategy (from 20% to 98% equities), but you don’t select individual funds. This is standard practice among other Pillar 3a providers too.

7

Interest rates offered by the Yuh account

YUH interest rates

YUH bank does not remunerate funds in CHF, EUR, and USD

8

Transfer speed with Yuh – sending money

YUH transfer speed

Instant transfers with “pay a friend” (from YUH user to YUH user).

An IBAN transfer within Switzerland made before noon arrives on the same day. If it’s done in the afternoon, it arrives the next day.

An international transfer (including SEPA) takes a maximum of 2 days.

9

YUH Twint – pay with TWINT anywhere in Switzerland

TWINT with YUH

Can You Use TWINT with Yuh?

Yes. Yuh has developed its own TWINT app, the #1 payment app in Switzerland. It lets you: – Pay in shops – Transfer money to friends – Split a bill within a group (restaurant, outings, etc.) – Pay for parking – Pay online and at train stations

YUH Bank charges: card, foreign exchange, transfers, cash withdrawals, etc.

YUH Bank fees

Free multi-currency account

IBAN CH free of charge

Free Mastercard Debit card

Replacement card CHF 20

Card payments without transaction fees (13 currencies included)

Exchange fees of 0.95% markup on the real interbank rate

Bank transfers

In Switzerland and Liechtenstein in 13 currencies: free

In Europe, SEPA transfers in EUR are free / other currencies 4 CHF

Cash withdrawals in Switzerland

At ATMs (cash dispensers): Free 1x/week then 1.90 CHF/withdrawal

Cash withdrawals abroad

At ATMs (classic dispensers): 4.90 CHF /withdrawal

Daily cash withdrawal limit of 1K CHF or 1K EUR.

You can change the monthly spending limit.

11

YUH on the road and abroad

Travelling abroad with YUH

In short, at YUH there are no transaction fees in the following currencies: CHF – USD – EUR – GBP – JPY – AUD – CAD – SEK – HKD – NOK – DKK – AED – SGD.

There is an exchange fee of 0.95%. This makes YUH an advantageous solution for travel, but not the most optimal for those who travel or cross the border frequently. In which case, competing offers such as Revolut and N26 may be more competitive.

€ / $ / £ Automatic multi-currency When abroad, Yuh pays with the right currency at the time of purchase, with no extra fees. If the currency is not available, the amount is debited in the currency with the most funds in the account, at the current YUH exchange rate.

📍Paying in local currency is always recommended.

This is possible even without funds in the currency account.

YUH instantly converts the most well-funded currency with standard fees

Yuh Promo Code

Use the promo code C9QK67 to receive 50 CHF in Trading Credit + 250 SWQ (with an initial deposit of CHF 500.-).

It’s free and easy to deposit cash to your YUH account via TWINT. You need to buy a refill at the Post Office, Coop or Interdiscount with the amount you wish to pay into your account.

13

YUH Bank Customer Service

Customer service

Accessibility: by phone 🤳 Monday to Friday from 8 AM to 10 PM, available in French, German, English, and Italian. You sometimes have to wait long minutes (18 min wait ⏳ during our last request). If you need quick answers on the weekend, you’ll have to settle for online help. This isn’t truly what neo-bank customers expect, even if the service is high quality.

From the YUH app via a form with the option of adding a screenshot to explain your problem.

There is no possibility to talk to a support person directly via chat from the app or the site.

Reported experience generally excellent. Even with technical questions, the efficiency is there. No guesswork. No stupid questions. Our last interaction was flawless (thanks Meriam). Support handles our issues precisely and conscientiously.

14

Cashback: YUH offers SQW to reward its users

Cashback: YUH rewards

YUH’s cashback is distributed via its Swissqoin (SWQ) cryptographic token.

You earn SWQ when you use the application.

SWQ is a crypto-token based on the Ethereum blockchain.

Yuh reinvests part of its income in it, so its value increases every month 📈.

Swissqoins can be exchanged for cash at any time

You can offer them to friends who are YUH customers

You can also keep your Swissqoins and wait for them to gain value.

15

Good reasons to open an account with YUH

Choosing YUH

The app. Yuh Bank is a complete solution well-suited to life in Switzerland: a free account in CHF and EUR, a free Mastercard, a CH IBAN, and eBill payments. This offer makes it one of the best options in and around Switzerland, as it is open to cross-border workers and non-residents.

Yuh allows you to pay in multiple currencies without changing cards, withdraw in EUR, and invest directly in ETFs or stocks. However, it doesn’t support LSV, nor some complex QR bills, and doesn’t offer a personal EUR IBAN. For a cross-border worker or someone juggling CHF and EUR, Yuh offers more flexibility than Neon. But for 100% Swiss usage, Neon remains more reliable for daily use.

if you stay in Switzerland, with CHF payments, QR bills, and need for clarity: Neon (read Neon review and test)

if you receive or spend in EUR, travel, or want to invest easily: Yuh

To avoid if…

you use TWINT regularly

if you receive payments in foreign currencies on a personal account

if you depend on local services like LSV

17

Yuh vs. Revolut – Quick Comparison ⚡️

Yuh VS. Revolut

Yuh vs Revolut

Revolut covers more international features, with better multi-currency support, competitive exchange rates, and more flexibility for payments abroad. However, the lack of a personal Swiss IBAN, incompatibility with QR-bills, and the inability to use TWINT make its daily use in Switzerland constraining.

Yuh bank, even with fewer global options, remains more balanced for regular use in CHF, while offering accessible investment functions.

if you live in Switzerland and want a solution capable of managing local expenses and some investments: Yuh

if you travel often, pay in multiple currencies, or look to optimize exchange fees: Revolut (read Revolut review and test)

To avoid if…

if you need a personal CH IBAN to receive a salary or make official payments

You use TWINT daily

if you’re looking for a simple interface without changing conditions depending on days or amounts

18

Yuh vs. Zak – Quick Comparison ⚡️

Yuh VS. Zak

Yuh vs Zak

Zak is better integrated into the Swiss banking environment: QR-bills, LSV, native TWINT, everything is in place for simple local use. But as soon as you leave the CHF zone, the limitations become visible: no multi-currency, fees on EUR withdrawals, no access to investment.

Yuh is less comprehensive for automatic payments but more versatile for those who alternate between Switzerland and the euro zone, or who want to invest part of their money.

To be preferred if…

you live in Switzerland and want a simple solution, compatible with TWINT and well integrated into the local ecosystem: Zak (read Zak review and test)

you travel regularly, receive or spend in EUR, or want to invest easily from the app: Yuh

To avoid if…

you depend on LSV or native access to TWINT (Yuh doesn’t support them)

you’re looking for a multi-currency bank (Zak only handles CHF)

you want an integrated savings or investment tool (non-existent with Zak)

Zak Promo Code

Use promo code KNSGS6 to receive CHF 25 when you open your account.

Alpian allows holding multiple currencies (CHF, EUR, USD, GBP) in a single account, with free international transfers and tailored investment management. However, it’s not possible to use TWINT, withdrawals in Switzerland are charged (2 CHF), and the physical card costs 60 CHF.

Yuh bank does not offer wealth management advice, but remains simpler to use for daily payments, mixed expenses in CHF/EUR and small ETF investments.

you’re looking for a simple tool to manage your payments, save or invest without entry conditions: Yuh

you have capital to invest and want to benefit from structured human guidance: Alpian (read Alpian review and test)

To avoid if…

you use TWINT regularly

you want a free card without fixed fees

you don’t intend to use the proposed investment functions

Alpian Promo Code

Use the promo code ALPHEY to receive 120 CHF (55 CHF with a deposit of 500 CHF within 30 days of account opening, and up to 65 CHF credit on investment fees).

N26 offers an efficient Mastercard for use abroad, with no conversion fees and simplified multi-currency management. However, it doesn’t provide a Swiss IBAN, which makes incoming transfers complex (salary, LSV) and prevents paying certain local bills. TWINT is not available.

Yuh bank is less competitive on international payments, but better integrated into Swiss practices and more versatile if you have income in CHF.

To be preferred if…

you live in Switzerland and need a CH IBAN to receive a salary or pay your bills: Yuh

Do you use Yuh as your main account or as a secondary account?

Is Yuh suitable for your needs abroad?

Share your feedback with all Neo’s friends 😈

8.5Expert Score

Review and Test of YUH Bank: Key Criteria

Yuh Review: The Best Online Bank in Switzerland? We compare all advantages... drawbacks... banking services... fees... features... tips... shortcomings... Use promo code C9QK67 to receive 50 CHF Trading Credit + 250 SWQ (with a first deposit of CHF 500.-).

Offering

8.5

Security

10

Opening an account

9

Bank card

8.5

Features

9

Interest rates

8.9

Transfer speed

9

TWINT

10

Fees

8.5

Abroad

9

Cash deposit

3

Customer service

8.8

Additional information

Specification: Yuh Bank – Review and Complete Analysis (March 2026) + get 50 CHF + 250 SQW

Online banking

Platforms

Android, iOS

Account

free

Currencies

CH, EUR, multi-currency

IBAN

CH

SEPA transfers

free

Trading

cryptocurrencies, ETF, stocks

Bank card

Bank card

Mastercard

Card type

Debit

Basic card

free

Replacement card

20 CHF

Card design

black, minimalist

Virtual card generation

yes

Withdrawals abroad (EUR)

CHF 4.90/withdrawal

Withdrawals in Switzerland (CHF)

Free 1x/week then CHF 1.90/withdrawal

For who?

Clients

individuals, Swiss cross-border commuters

Minimum age

18 years old

Country of residence

Austria, France, Germany, Italy, Liechtenstein, Switzerland, United Kingdom

Mobile payments

Mobile platforms

Apple Pay, Google Pay, Samsung Pay

Reviews (1)

1 review for Yuh Bank – Review and Complete Analysis (March 2026) + get 50 CHF + 250 SQW

5.0out of 5

★★★★★

★★★★★

0

★★★★★

0

★★★★★

0

★★★★★

0

★★★★★

0

Write a review

Show allMost HelpfulHighest RatingLowest Rating

★★★★★

Gisela A –

Cet avis est complet merci ! Je vais sûrement choisir celle-ci pour moi et ma fille.

Gisela A –

Cet avis est complet merci ! Je vais sûrement choisir celle-ci pour moi et ma fille.